Paying a fee to “roll over” your payday loan feels like buying time, but in reality, you’re just purchasing a more expensive version of the same crisis. When you’re staring at a dwindling bank account and the fear of an automatic ACH withdrawal emptying your next paycheck, a renewal seems like the only way to survive the week. It’s a heavy burden to carry. You’re likely exhausted from the constant stress of managing multiple lenders who don’t care about your financial stability. If you’ve been searching for payday loan rollover help, you deserve to know that there’s a significant difference between a predatory delay and a permanent solution.

This article explores how to distinguish between these traps and the legitimate path to freedom found in payday loan consolidation. You’ll learn how to stop the cycle of endless fees and combine those scattered payments into one manageable amount. We’re going to examine why 2026 lending trends make consolidation the smarter choice and give you the tools to finally regain control over your bank account.

Learn how to identify the “relief trap” of payday loan rollovers, which offer a temporary sense of safety while keeping your principal balance untouched. We break down the math showing how fees can quickly outpace your original loan, proving why a structured exit strategy is more effective than a simple renewal.

Discover immediate payday loan rollover help by following our guide to revoking ACH authorizations and requesting Extended Repayment Plans to protect your income. You’ll also explore how payday loan consolidation and relief programs provide a permanent resolution to high-interest debt, helping you regain control of your bank account and your peace of mind.

What is a Payday Loan Rollover and Why Does It Feel Like Help?

That sudden wave of calm you feel when a lender offers to push back your due date is a carefully engineered mirage. When you’re struggling to find payday loan rollover help, the offer to pay a small fee instead of the full balance feels like a lifeline. In reality, a rollover is simply the act of paying the interest or a flat fee to extend a loan’s due date without reducing the principal balance by a single cent. You aren’t paying down your debt; you’re merely paying for the privilege of keeping it for another two weeks.

This “relief trap” is effective because it targets your immediate survival instincts. In the high-interest landscape of 2026, where average APRs still hover around 391 percent, lenders know that “buying time” is the most expensive product they sell. They profit most when you’re stuck in a holding pattern. While a rollover provides a temporary sense of safety, it ensures that your next paycheck is already spoken for before you even receive it. It’s a cycle designed to keep your bank account in a state of perpetual exhaustion.

The Mechanics of the Renewal Cycle

Lenders often frame these extensions as a “courtesy” or a “service” to help you avoid a default. It’s vital to understand the vocabulary they use to mask the cost. What is a Payday Loan Rollover exactly? While terms like “rollover,” “renewal,” and “refinance” are used interchangeably, they all lead to the same result. A rollover generally refers to paying a fee to delay the current loan. A renewal often involves a new contract that replaces the old one. A refinance might even add more principal to the total. In every scenario, your original debt remains untouched while the total amount you’ve paid grows exponentially.

The Psychological Impact of Perpetual Debt

The stress of a looming “failed payment” or an empty bank account can cloud your long-term judgment. Lenders count on this anxiety to drive quick, high-cost decisions. You might feel a sense of obligation to keep paying fees because you’ve already invested so much money into the loan. This is a dangerous mental trap that keeps you tethered to a predatory lender long after you should have found a way out. The sunk cost fallacy in payday lending is the mistaken belief that you must continue paying rollover fees simply because you’ve already spent hundreds of dollars trying to keep the loan afloat. Breaking this cycle requires recognizing that the money spent on fees is gone, but your future income can still be saved through a structured resolution.

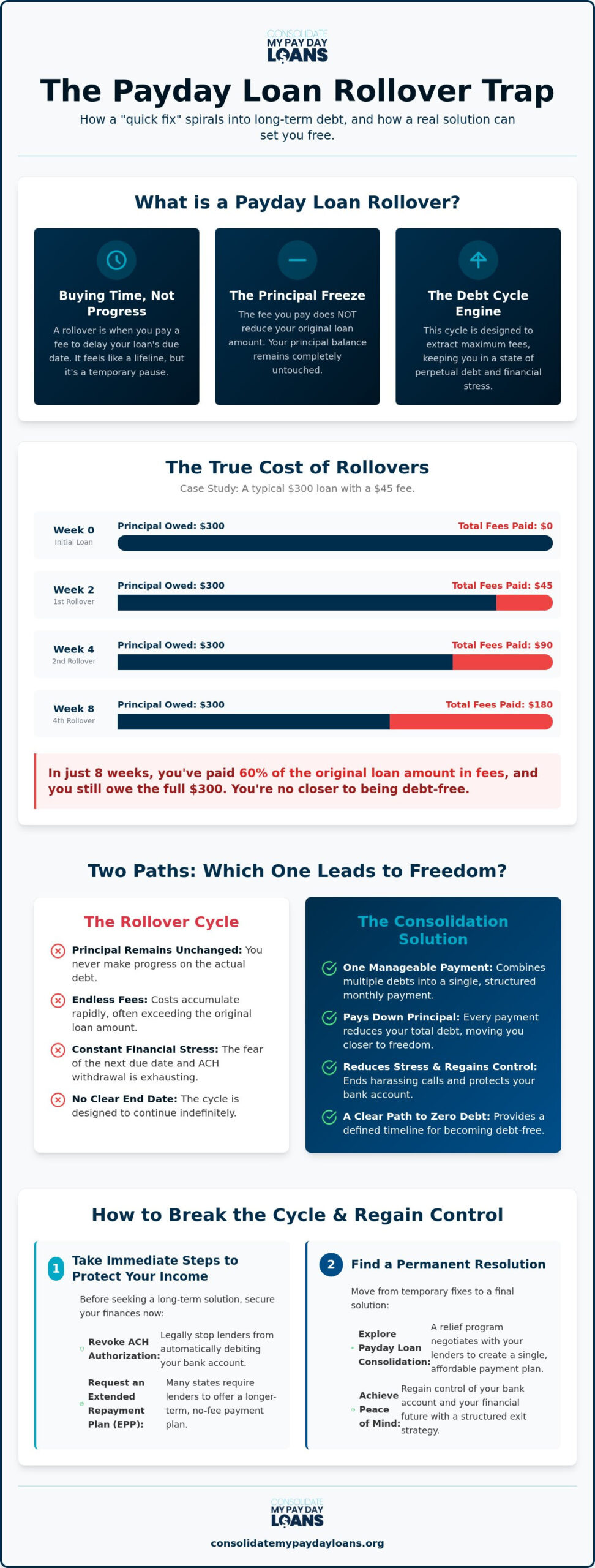

The True Cost of Rollovers: Comparing the Math of the Debt Trap

Numbers don’t lie, even when lenders try to hide them behind the promise of a “quick fix.” A typical payday fee ranges between $15 and $30 for every $100 you borrow. While this might seem manageable as a one-time emergency expense, the math changes the moment you can’t pay the full balance on your next payday. According to the Consumer Financial Protection Bureau, The True Cost of Rollovers is revealed by the fact that four out of five payday loans are either rolled over or renewed within 14 days. When you’re searching for payday loan rollover help, you’re usually trying to stop a financial leak that’s already become a flood.

Think of this cycle as a “Principal Freeze.” When you pay a rollover fee, you’re essentially paying the lender to keep your debt exactly where it is. Not a single penny of that fee goes toward the amount you actually borrowed. If you roll over a loan just three times, you’ll often find you’ve paid more in fees than the original loan was worth. You can use a payday loan consolidation calculator to see exactly how much your current cycle is costing you in real-time. Seeing the numbers clearly is often the first step toward breaking the cycle.

The $300 Loan Case Study

Imagine you borrow $300 with a standard $15 fee per $100. Your initial cost is $45. If you can’t pay the full $345 in two weeks, you pay another $45 to roll it over. By the end of eight weeks, you’ve paid $180 in fees alone. You still owe the original $300. In this scenario, your total cost of borrowing has reached 60 percent of the loan amount in just two months, yet you’re no closer to being debt-free. In states with high average APRs like Idaho, where borrowing $500 can cost an extra $1,000 in interest, this math becomes even more predatory. The 2026 reality remains harsh: short-term renewals are designed to be long-term profit centers for the lender.

Hidden Fees Beyond the Rollover

The trap doesn’t stop at the rollover fee. If your bank account doesn’t have enough to cover the fee, you’ll likely face a Non-Sufficient Funds (NSF) fee from your bank. Simultaneously, the lender may charge a late fee or a failed payment fee. These costs stack up rapidly, especially if you have multiple loans rolling over on the same day. It’s a compounding crisis that can drain a bank account in hours. If you’re tired of watching your hard-earned money disappear into a void of fees, it’s worth taking a moment to explore consolidation options that actually target your principal balance and offer a clear end date.

Rollover vs. Consolidation: Which Path Actually Leads to Freedom?

Choosing between a rollover and consolidation is like choosing between treading water and swimming toward the shore. A rollover buys you exactly 14 days of silence from your lender, but it doesn’t reduce what you owe. It’s a temporary band-aid on a deep financial wound. Consolidation, however, is a structured exit strategy that stops the bleeding. While rollovers focus on delaying the inevitable, consolidation is designed to eliminate the principal balance once and for all. You move from paying a large, recurring fee that vanishes into the lender’s pocket to making one manageable payment that actually reduces your debt. For a deeper look at how this transition works, you can read our Payday Loan Consolidation: The Complete Guide.

The difference in your monthly cash flow is immediate. When you seek payday loan rollover help, you’re often just trying to prevent your bank account from hitting zero on Friday. Consolidation changes the math by grouping multiple high-interest obligations into a single, predictable monthly amount. This shift allows you to breathe again. Instead of wondering which lender will hit your account first, you follow a clear path toward a zero balance. It’s the difference between surviving the week and planning for next year.

Short-Term Delay vs. Long-Term Strategy

Rollovers are fundamentally reactive. They’re a response to the panic of an upcoming due date. This reactive cycle forces you into the “borrowing from Peter to pay Paul” trap, where you take out new loans just to cover the fees of the old ones. This cycle quickly drains the funds you need for essentials like rent, food, and utilities. Consolidation is a proactive choice. It’s a decision to stop playing by the lender’s rules and start following a methodology that prioritizes your financial recovery. By stabilizing your payments, you regain the ability to cover your daily living expenses without fear.

The Impact on Your Credit and Future

Endless rollovers eventually lead to a breaking point. When the fees become too high to cover, many borrowers face a default that can severely damage their credit standing for years. Professional relief programs offer a way to stabilize your situation before that collapse happens. In 2026, lenders are increasingly willing to negotiate with professional consolidation services because they prefer a structured repayment over a total loss. Working with a dedicated advocate shows lenders you’re committed to resolution, which often leads to better terms and a faster path to psychological peace.

Immediate Steps to Stop Rollovers and Protect Your Bank Account

The cycle of debt often feels like it has its own momentum. To stop it, you must take deliberate actions that shift the power back to your own hands. Finding effective payday loan rollover help starts with securing your income before the next withdrawal hits. This isn’t about running away from your obligations; it’s about creating the breathing room necessary to resolve them properly. Follow these four steps to interrupt the cycle today.

- Step 1: Revoke ACH authorization. This is your most powerful tool for immediate protection. It stops lenders from reaching into your account the moment your paycheck lands.

- Step 2: Request an Extended Repayment Plan (EPP). Many states and industry associations require lenders to offer a no-cost extension if you ask for it before the due date.

- Step 3: Organize your documents. Gather every contract and receipt to calculate your total “rollover damage.” Seeing the total amount spent on fees versus the original principal provides the clarity needed for a final resolution.

- Step 4: Seek professional guidance. Contacting an expert for payday loan relief can help you transition from temporary delays to a permanent exit strategy.

Your Legal Right to Revoke ACH Authorization

You don’t need a lender’s permission to stop an automatic withdrawal. Federal law gives you the right to revoke your authorization for electronic transfers at any time. To do this, you must notify the lender in writing that you are revoking their access to your account. Simultaneously, you should contact your bank and provide them with a copy of that notice. While most banks allow you to place a “stop payment” on a specific transaction, a full revocation of authorization is more comprehensive. Revoking ACH does not cancel the debt, but it gives you control over timing and ensures you can prioritize essentials like rent and food.

How to Ask for an Extended Payment Plan (EPP)

In states like Florida, Michigan, and California, specific regulations exist to help borrowers who cannot repay on time. Even in states without strict mandates, many lenders will offer an EPP to avoid a total default. The “magic words” are simple: “I am unable to pay this loan in full and I am requesting an Extended Payment Plan as a member of the CFSA or under state law.” You must usually make this request at least one business day before the loan is due. If a lender refuses to offer a hardship program despite legal requirements, don’t argue with them. Document the refusal and start your recovery today by speaking with a professional advocate who knows how to handle non-compliant lenders.

Moving Toward Resolution: How Payday Loan Relief Programs Work

Resolution begins the moment you decide that the next fee you pay will be your last. Payday loan relief programs serve as a structured alternative to the rollover trap, transforming a chaotic series of deadlines into a predictable path toward a zero balance. While a rollover keeps you in a state of financial suspension, professional relief programs actively dismantle the debt. Expert negotiators work directly with your lenders to stop the accumulation of interest and predatory fees. This process shifts the focus from survival to settlement. By consolidating your obligations, you move to a single monthly payment designed to fit your actual budget rather than the lender’s profit margins. If you are tired of the cycle, you can get a free debt analysis today and stop the rollover cycle for good.

Finding effective payday loan rollover help means looking beyond the next two weeks. Professional relief isn’t just about merging numbers; it’s about changing the terms of your engagement with the lending industry. In 2026, the landscape of short-term lending remains aggressive, but lenders are often more willing to settle with a third-party advocate than with an individual borrower. This advocacy provides a buffer between your bank account and the lenders, allowing you to regain your financial agency while your debt is systematically reduced.

Regaining Your Financial Agency

The burden of high-interest debt is as much mental as it is financial. Having a professional advocate on your side provides immediate psychological relief. You no longer have to field aggressive collection calls or spend your nights worrying about which lender will empty your account first. Consolidation programs allow you to focus on one goal rather than fighting multiple fires simultaneously. Most structured relief plans provide a clear, documented timeline for becoming debt-free. This clarity replaces the “perpetual debt” feeling with a sense of momentum. Instead of treading water, you are finally moving toward the shore.

Is Consolidation Right for You?

Not every financial struggle requires a formal relief program, but certain patterns indicate that you need professional intervention. You are likely a candidate for payday loan relief if you meet the following criteria:

- You have two or more payday loans currently open.

- You have rolled over at least one loan more than twice in the last 60 days.

- The total fees you pay each month exceed the amount you can afford for basic living expenses.

- You are considering taking out a new loan just to cover the interest on an existing one.

It is also beneficial to consider a unified exit strategy that includes credit card consolidation. High-interest credit cards often compound the problem, creating a web of debt that feels impossible to untangle. 2026 is the year to finally break this predatory cycle. By addressing all your high-cost obligations at once, you simplify your financial life and protect your future income from further erosion. The path to freedom is through structure, not through another 14-day delay.

Reclaim Your Financial Future Today

The cycle of debt thrives on the fear that there is no other way out. As we’ve explored, a rollover is never a courtesy; it’s a premium price for a temporary delay that leaves your principal balance untouched. By understanding the math of the debt trap and taking immediate steps like revoking ACH authorization, you’ve already begun the process of protecting your bank account. Real payday loan rollover help isn’t about finding another way to pay a fee. It’s about implementing a structured exit strategy that prioritizes your stability over a lender’s profit.

With over 20 years of debt management expertise and national service coverage across the United States, our team specializes in providing the specialized payday loan relief you need to break free. You don’t have to manage these multiple lenders and constant stress on your own anymore. It’s time to move toward a resolution that fits your actual budget and offers a clear end date. Break the rollover cycle with a single-payment consolidation plan. You’ve carried this burden long enough; let’s start the path toward your psychological peace and financial recovery today.

Frequently Asked Questions

What is the difference between a payday loan rollover and a renewal?

A rollover involves paying a fee to delay the due date of an existing loan, while a renewal often involves creating a new loan contract to pay off the old one. Both tactics keep you in debt without reducing the principal. In 2026, these terms are often used interchangeably by lenders to mask the compounding costs. Neither option helps you reach a zero balance because they only address the interest or service fees.

Can I stop my payday lender from rolling over my loan automatically?

Yes, you can stop a lender from rolling over your loan by providing written notice that you intend to pay the balance or enter a repayment plan. You should also check your original contract for any auto-renewal clauses that you can opt out of. If you need immediate payday loan rollover help, revoking your payment authorization is the most effective way to prevent unauthorized extensions and fees from hitting your account.

How many times can a payday lender legally roll over a loan in 2026?

The number of legal rollovers varies significantly by state in 2026. For example, states like Florida, Michigan, and California strictly prohibit rollovers and renewals entirely. Conversely, states like Idaho and Utah have much more permissive regulations. You must check your specific state’s consumer protection laws to see if your lender is exceeding the legal limit for renewals or if they are operating in a state where the practice is banned.

Does rolling over a payday loan help my credit score?

Rolling over a payday loan does not help your credit score because most payday lenders don’t report on-time payments to the major credit bureaus. However, the cycle of rollovers often leads to a default, which will severely damage your credit. The only way to improve your financial standing is to resolve the debt entirely through a structured plan rather than continuing to pay for temporary delays that offer no long-term benefit.

What happens if I cannot afford the rollover fee this month?

If you cannot afford the rollover fee, you should immediately request an Extended Repayment Plan (EPP) before your next due date. In many jurisdictions, lenders are required to offer this no-cost extension to borrowers facing financial hardship. If an EPP isn’t available, seeking professional assistance to consolidate your debt can stop the accumulation of fees and prevent the lender from emptying your bank account through failed payment attempts and bank charges.

Is a payday loan consolidation program better than a rollover?

A payday loan consolidation program is superior to a rollover because it focuses on eliminating the principal balance rather than just delaying the due date. Rollovers are designed to keep you paying fees indefinitely. Consolidation merges your high-interest debts into one manageable payment with a clear end date. This approach provides the psychological peace of knowing your debt is actually shrinking every month instead of staying frozen in a cycle of renewals.

Can I get payday loan rollover help if I have multiple loans?

You can absolutely get payday loan rollover help even if you are juggling multiple lenders simultaneously. In fact, consolidation is specifically designed for individuals facing the stress of several different payment schedules. By grouping all your loans into a single relief program, you stop the cycle of borrowing from one lender to pay another. This simplification allows you to regain control over your income and ensures that no single lender can trigger a chain reaction of bank fees.

How do I legally stop ACH withdrawals from a payday lender?

To legally stop ACH withdrawals, you must notify the lender in writing that you are revoking their authorization to debit your account. Under federal law, you have the right to stop these transfers at any time. You should also send a copy of this revocation to your bank to ensure they block any future attempts. This action gives you control over your cash flow, though it’s important to remember that revoking access does not eliminate the underlying debt you still owe.