If your credit card interest rates have climbed toward 25.16 percent, are you actually paying off your balance or just funding a bank’s profit margin? It’s a heavy burden to carry, and it’s natural to feel like you’re running in place while high interest eats away at your progress. You’re likely tired of the anxiety that comes with juggling multiple due dates and the fear that your credit score might never fully recover. We understand that this pressure feels overwhelming, but you don’t have to face it without a map.

If you’re asking yourself, “should i consolidate my credit card debt,” you aren’t just looking for a lower payment. You’re looking for a way to reclaim your financial agency. This comprehensive 2026 guide will help you determine if consolidation is the right financial reset for your unique situation. You’ll learn how to build a strategic exit plan using the latest tools, such as 21-month 0 percent APR offers or personal loans for those with excellent credit. We will break down the mechanics of these financial processes so you can stop the cycle of debt and start a clear, methodical path toward psychological peace.

Key Takeaways

- Learn to identify the “debt treadmill” effect where high interest rates keep your balances stagnant despite making regular monthly payments.

- Evaluate the specific financial markers that help you decide “should i consolidate my credit card debt” to lower your overall interest costs.

- Understand the balance between immediate relief and long-term discipline, including how to avoid the common trap of accumulating new debt after consolidating.

- Compare modern consolidation vehicles like 0% APR balance transfers and personal loans to find the most effective tool for your credit profile.

- Discover how to integrate your credit card strategy with a broader plan for payday loan relief to reclaim your full financial agency.

Recognizing the Signs: When Credit Card Consolidation Makes Sense

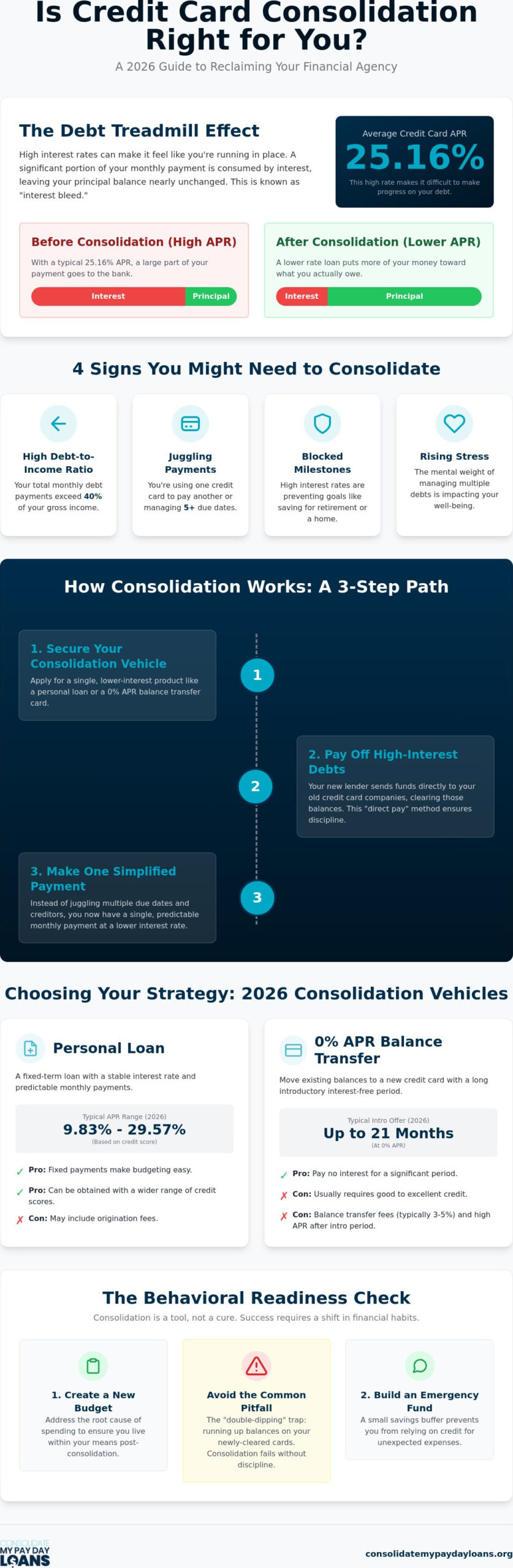

You might feel like you’re walking on a treadmill that’s slowly accelerating. You make your payments every month, yet the balance barely budges. In 2026, with average credit card interest rates reaching 25.16 percent, this isn’t just a feeling; it’s a mathematical reality for many households. When you’re asking yourself, “should i consolidate my credit card debt,” you’re usually at a point where the mental weight of five or more monthly due dates is becoming unbearable. Managing multiple high-interest accounts creates a constant state of low-level panic that drains your energy and distracts you from your long-term goals. If your debt-to-income ratio is creeping toward the 40 percent mark, you’re approaching a critical threshold where traditional repayment may no longer be viable.

The Mathematical Turning Point

There’s a specific “20% Rule” we use to identify when a financial situation has become unsustainable. If your interest rates exceed your ability to pay down the principal by more than 20 percent each month, you’re experiencing what we call “interest bleed.” This is the point where your hard-earned money is effectively vanishing into the bank’s coffers rather than reducing what you owe. The exact moment when interest costs outweigh principal reduction marks the transition from a manageable obligation to a systemic trap. Utilizing a Debt consolidation strategy or a specialized calculator can help you visualize this bleed and see exactly how much time and money you’re losing to the status quo.

The Behavioral Readiness Check

Consolidation is a powerful tool for recovery, but it isn’t a magic wand. Before you decide “should i consolidate my credit card debt,” you must evaluate if you’ve addressed the root cause of the credit card spending. Consolidation often fails if it isn’t paired with a firm commitment to a new budget and the establishment of a modest emergency fund. Without these safeguards, you risk the common pitfall of “double-dipping,” which involves paying off the cards only to run them back up again because of an unexpected expense. True recovery requires both a financial reset and a behavioral shift. We advocate for a methodical approach that prioritizes your psychological peace and ensures you have the agency to stay debt-free for good.

To determine if you’re ready for this step, consider these indicators:

- Your total monthly debt payments exceed 40 percent of your gross income.

- You’re consistently using one credit card to pay for the minimum balance on another.

- High interest rates are preventing you from reaching 2026 financial milestones like home ownership or retirement savings.

- The stress of managing multiple creditors is impacting your physical health or personal relationships.

How Credit Card Debt Consolidation Works in 2026

Deciding should i consolidate my credit card debt involves more than just looking at your monthly bill; it is about understanding how a new financial structure can stop the interest bleed. At its core, consolidation is the process of taking several high-interest debts and rolling them into one new obligation with a lower interest rate. This strategy replaces the chaos of multiple creditors with a single, structured monthly payment. In 2026, the primary goal is to escape the 25.16 percent average credit card APR by finding a more efficient “consolidation vehicle.” This vehicle could be a personal loan, a specialized debt management plan, or a relief program designed to lower your overall cost of borrowing.

The current financial environment makes your choice of vehicle critical to your success. For example, as of July 2026, those with excellent credit can secure personal loan APRs as low as 9.83 percent, while those with poor credit may see rates near 29.57 percent. If you are still weighing should i consolidate my credit card debt, consider the gap between your current rates and the lower APRs available through consolidate credit card debt strategies. When you secure a lower rate, more of your payment goes toward the principal balance instead of disappearing into interest charges. This shift allows you to pay off the same amount of debt in a fraction of the time.

The Mechanics of Debt Transfer

The process begins once your application for a consolidation vehicle is approved. Many modern lenders offer “direct pay” options, which we highly recommend for maintaining discipline. With direct pay, the new lender sends funds directly to your old credit card companies to pay off your balances. This removes the temptation to spend the loan proceeds on other expenses. The timeline is typically efficient, as most accounts are settled within seven to ten business days. Once the balances hit zero, you transition to making just one monthly payment to your new provider. If you find yourself struggling with various types of high-cost debt, using a payday loan consolidation calculator can help you visualize how these different obligations can be streamlined into one manageable plan.

Impact on Your Credit Profile

It is natural to worry about your credit score during this transition. You will likely see a temporary dip of five to ten points due to the hard credit inquiry and the opening of a new account. However, this is a short-term trade-off for a long-term gain. By paying off revolving balances, you drastically lower your credit utilization ratio. Lowering the percentage of available credit you are using is one of the fastest ways to build a resilient score. Reducing your credit utilization ratio to under 30 percent serves as a powerful signal to FICO’s 2026 algorithms that you are managing your financial agency responsibly. Over time, your consistent, on-time payments to the single consolidation account will create a stable history that far outweighs the initial inquiry.

Evaluating the Pros and Cons: Is It the Right Move for You?

Deciding should i consolidate my credit card debt requires a cold, hard look at your financial numbers versus your current emotional state. The immediate relief of a lower monthly payment is seductive, but you must ensure you aren’t simply trading one burden for another that lasts twice as long. A strategic reset only works if the total cost of the new loan or plan is lower than the path you are currently on. This evaluation is the most critical step in regaining your financial agency. You need to verify that the math supports your hope for a fresh start.

Before moving forward, it is essential to consult the Consumer Financial Protection Bureau on debt consolidation to understand the standard protections available to you. While legitimate programs offer a lifeline, the industry is unfortunately populated by predatory actors. Be wary of any company that demands significant upfront fees before they have performed any services or negotiated with your creditors. Legitimate consolidation is a transparent process, not a collection of “secret” loopholes or overnight miracles. If a deal feels too good to be true, it likely is.

The Benefits of a Strategic Reset

The primary advantage of consolidation is the immediate improvement in your 2026 monthly cash flow. By moving away from “revolving” uncertainty, you establish a fixed end date for your debt. This predictability acts as a financial anchor, providing the mental clarity needed to focus on other goals. Instead of managing the average household credit card debt of $6,715 across multiple high-interest accounts, you face a single, manageable obligation. This simplification reduces the cognitive load and anxiety associated with juggling numerous due dates and fluctuating minimum payments.

Potential Drawbacks and Risks

One of the most significant risks is “double-dipping,” where a consumer pays off their cards with a loan but continues to use the original credit lines for new purchases. This behavior can lead to a debt load that is twice as heavy as before. You must also account for origination fees, which can range from 1 percent to 8 percent of the total loan value, potentially eating into your savings. Additionally, extending your repayment term might lower your monthly bill, but it could result in paying more total interest over the life of the loan. For a deeper look at managing your accounts during this time, read our Can I Still Use My Credit Card After Debt Consolidation? (2026 Guide). We encourage you to be tough on the systemic problem of high-interest lending while remaining compassionate toward your own need for a sustainable recovery.

Choosing Your Strategy: Loans, Balance Transfers, and Relief Programs

Selecting the right vehicle for your recovery depends entirely on your current credit standing and total debt load. If you are asking should i consolidate my credit card debt, you must first identify which category of borrower you fall into. For those with excellent credit, typically a score of 740 or higher, the most efficient tool is often a 0 percent introductory APR balance transfer card. These offers provide a window of up to 21 months to attack the principal balance without any new interest accruing. You must, however, factor in a transfer fee that usually ranges from 3 percent to 5 percent of the total amount. If your credit is in the middle market, a personal consolidation loan provides a fixed interest rate and a structured payoff date that revolving credit simply cannot match.

When a Loan is the Best Path

A personal loan is the preferred choice when you want to lock in a stable rate and move away from the uncertainty of variable credit card APRs. To qualify for the most competitive 2026 rates, which can be as low as 9.83 percent for those with excellent credit, lenders will look for a stable income and a manageable debt-to-income ratio. It’s vital to compare the Annual Percentage Rate (APR) rather than just the simple interest rate; the APR includes origination fees that can significantly impact your total cost. While unsecured loans are standard, they often come with higher rates for those with “fair” credit, where APRs can reach 28.93 percent. We recommend evaluating these costs carefully to ensure the loan actually reduces your financial burden.

When Debt Relief is the Safer Alternative

For individuals with high debt-to-income ratios or credit scores below 580, a new loan may be out of reach or come with rates exceeding 29 percent. In these cases, debt relief or a structured negotiation plan becomes the safer alternative. These programs focus on working directly with your existing creditors to lower interest rates and waive late fees without requiring you to take on a new loan. This approach is especially effective if you are also struggling with other high-cost traps. You can explore how to combine these efforts in our guide on Credit Card and Payday Loan Consolidation: A Unified Exit Strategy for 2026. Negotiation provides a path forward for those the traditional banking system often leaves behind.

If you’re ready to stop the cycle of high-interest debt and regain your financial agency, start your credit card consolidation plan today and take the first step toward psychological peace.

Beyond the Cards: Creating a Unified Debt Exit Plan

Focusing solely on credit cards is a common mistake that can sabotage your broader financial recovery. If you are asking should i consolidate my credit card debt, you must also look at other high-interest traps that might be draining your monthly income. Predatory lending, particularly in the form of payday loans, often exists alongside credit card debt, creating a compounding cycle of interest that is nearly impossible to break through traditional payments alone. To achieve true psychological peace, your strategy must address every predatory obligation you carry. Treating these debts in isolation is like patching one hole in a sinking boat while ignoring several others; you need a comprehensive plan to stay afloat.

The most effective way to reclaim your agency is to integrate your credit card strategy with a payday loan consolidation plan. This approach ensures that you are not just moving money around, but systematically dismantling every high-cost barrier to your success. By viewing your debt as a single systemic problem rather than a collection of individual bills, you can apply a methodical methodology to your recovery. This unified path allows you to stop the interest bleed across all accounts simultaneously, moving you closer to a debt-free life in 2026.

Managing Multiple Debt Types Simultaneously

A unified strategy is significantly more effective than piecemeal consolidation because it allows you to prioritize obligations based on their total cost and predatory terms. While credit card rates are high, payday loans can carry APRs that dwarf even the most expensive cards. We advocate for a structured hierarchy of repayment where the most damaging debts are neutralized first. Having a single advocate for all your unsecured obligations provides a stable anchor during this transition. It simplifies your communication with creditors and ensures that no single lender can derail your progress with aggressive collection tactics or hidden fees.

Securing Your Financial Future

Once you have established your consolidation plan, the focus shifts to maintaining your momentum. Consistency is the foundation of recovery, so we recommend setting up automated payments to ensure you never miss a due date. This automation removes the monthly stress of manual management and helps your credit score recover more predictably as you move through 2026. Monitoring your progress is essential; seeing your principal balances drop each month provides the tangible proof of improvement that keeps you motivated. You have the power to stop the cycle of debt and build a future defined by agency rather than obligation. Calculate your potential savings and take the first step toward relief.

Reclaiming Your Financial Agency in 2026

You have analyzed the numbers and assessed your readiness. Deciding should i consolidate my credit card debt is the first step toward stopping the interest bleed and regaining your psychological peace. A successful reset relies on choosing the right vehicle, whether it’s a 0 percent balance transfer for those with excellent credit or a structured relief program for those facing higher debt-to-income ratios. By addressing your high-interest credit cards alongside any predatory payday loans, you create a unified exit plan that protects your long-term stability.

At Consolidate My Payday Loans, we have provided empathetic, non-judgmental support since 2004. With over 20 years of expertise, we specialize in offering relief for high-interest and predatory debt that traditional banks often ignore. You don’t have to face this financial turbulence alone. Start your journey to financial peace with our Debt Consolidation Calculator and visualize your path to recovery today. You have the power to break the cycle and build a future defined by your own choices.

Frequently Asked Questions

Does consolidating my credit card debt hurt my credit score?

Consolidating your debt typically causes a small, temporary dip in your credit score due to the hard inquiry and the opening of a new account. However, this is a short-term trade-off for a significant long-term gain. By paying off revolving balances, you drastically lower your credit utilization ratio, which is a key factor in building a resilient score. Most individuals who are asking should i consolidate my credit card debt find that their scores recover and even improve within six to twelve months of consistent, on-time payments.

Is it better to get a consolidation loan or use a balance transfer card?

The choice between a loan and a balance transfer card depends on your credit score and how much time you need to pay off the balance. Balance transfer cards are excellent if you have a score above 740 and can realistically pay off the debt within a 0 percent APR introductory period of 15 to 21 months. If you need more time or have a middle-market credit score, a personal consolidation loan provides a fixed interest rate and a structured payoff date that offers more stability and psychological peace.

Can I consolidate my credit cards if I also have payday loans?

Yes, you can and should integrate your credit cards into a unified strategy if you are also struggling with payday loans. We specialize in merging these different high-cost obligations into a single, manageable plan that addresses the most predatory interest rates first. Treating these debts in isolation often fails because the extreme costs of payday lending sabotage your ability to pay down credit card principal. A unified path ensures that every dollar you pay works toward your total recovery.

How much can I actually save by consolidating my debt in 2026?

Your total savings depend on the gap between your current interest rates and your new consolidation rate. With 2026 credit card APRs averaging 25.16 percent, the potential for reduction is substantial if you qualify for a loan at 11.92 percent or a 0 percent transfer offer. Reducing the interest bleed ensures that more of your payment goes directly toward the principal balance. This shift can save you thousands of dollars in interest charges over the life of your debt while shortening your repayment timeline by years.

What happens to my credit cards once they are consolidated?

Once your debt is consolidated, the new lender or program pays off your original credit card balances, bringing them to zero. You generally don’t have to close the accounts, and keeping them open can actually benefit your credit score by maintaining the length of your credit history. However, you must have the discipline to stop using those cards for new purchases. The goal is to move away from revolving uncertainty and toward a fixed, predictable end date for your financial obligations.

Are there legitimate debt consolidation programs for people with bad credit?

Legitimate consolidation programs exist even for those with credit scores below 580 who may not qualify for traditional bank loans. Instead of a new loan, these programs use structured negotiation to lower interest rates and waive fees on your existing accounts. This approach is a safer alternative for those with high debt-to-income ratios who need an advocate to help them navigate complex financial traps. We provide the expertise needed to negotiate with lenders and create a methodical path toward improvement.

How long does the debt consolidation process usually take?

The initial setup for a consolidation plan or loan typically takes seven to ten business days from the time your application is approved. Once the funds are disbursed or the negotiation is finalized, you transition immediately to a single monthly payment. The total time to reach a zero balance depends on your specific plan structure, with most programs designed to be completed within 24 to 60 months. This structured approach ensures that the process is predictable and builds your confidence over time.

Can I still use my credit cards while I am in a consolidation program?

Continuing to use your credit cards while in a consolidation program is generally discouraged because it creates a risk of “double-dipping.” Adding new debt while trying to pay off the old balance creates a heavier burden and can lead to systemic failure. To regain your financial agency, it’s essential to commit to a new budget and stop using revolving credit lines during your recovery. Focusing on a single, predictable financial anchor is the most effective way to reach your 2026 financial goals.