What if your bank account didn’t hit zero the moment your paycheck arrived? You’re likely exhausted by the relentless cycle of triple-digit interest rates and lenders who seem to have more control over your money than you do. It’s a heavy burden when average payday loan APRs in 2026 hover around 391%, and lenders use ACH access to drain your funds before you can pay for essentials. You deserve a way to lower payday loan payments and regain your psychological peace. We understand the pressure of multiple lenders calling and the feeling of being trapped by high-interest rollovers that never seem to end.

This guide provides a clear path toward relief by detailing proven strategies and professional programs that actually work. You’ll discover how to shift from predatory lump-sum demands to structured, interest-reduced installments that fit your actual budget. We’ll explain the process of stopping automatic bank withdrawals and consolidating your obligations into a single, lower monthly payment. By the end of this article, you’ll have a step-by-step methodology to break the debt cycle and establish a firm end date for your financial recovery.

Key Takeaways

- Identify the mechanics of the “lump-sum” model and how rollover fees are specifically designed to prevent you from ever touching the loan’s principal balance.

- Learn the immediate steps to lower payday loan payments by formally requesting an Extended Payment Plan (EPP) at least two days before your next scheduled withdrawal.

- Evaluate the critical differences between debt settlement and professional consolidation to choose a strategy that provides a clear end date for your debt.

- Understand why a professional management plan is not a new loan, but a structured way to pool multiple lenders into one predictable monthly disbursement.

- Discover how to use a payday loan consolidation calculator to visualize your potential savings and reclaim agency over your financial future.

Why Payday Loan Payments Are So High (and Why They Keep Growing)

Most financial products are built to be repaid over months or years. Payday loans operate on a different, more aggressive logic. They rely on a lump-sum repayment model. This means the lender expects the entire principal plus interest back within 14 to 30 days. It’s a structure that sets many borrowers up for failure from the start. When a massive portion of your paycheck disappears instantly, it’s nearly impossible to cover your remaining bills. This pressure is why so many people look for ways to lower payday loan payments before their bank account hits zero.

The timing of these payments adds another layer of difficulty. Because lenders sync withdrawals with your bi-weekly pay cycle, the money is often gone before you can buy groceries or pay rent. This creates a vacuum in your monthly household budget that usually leads to borrowing again just to survive the next week. It’s a cycle designed for the lender’s profit, not your recovery.

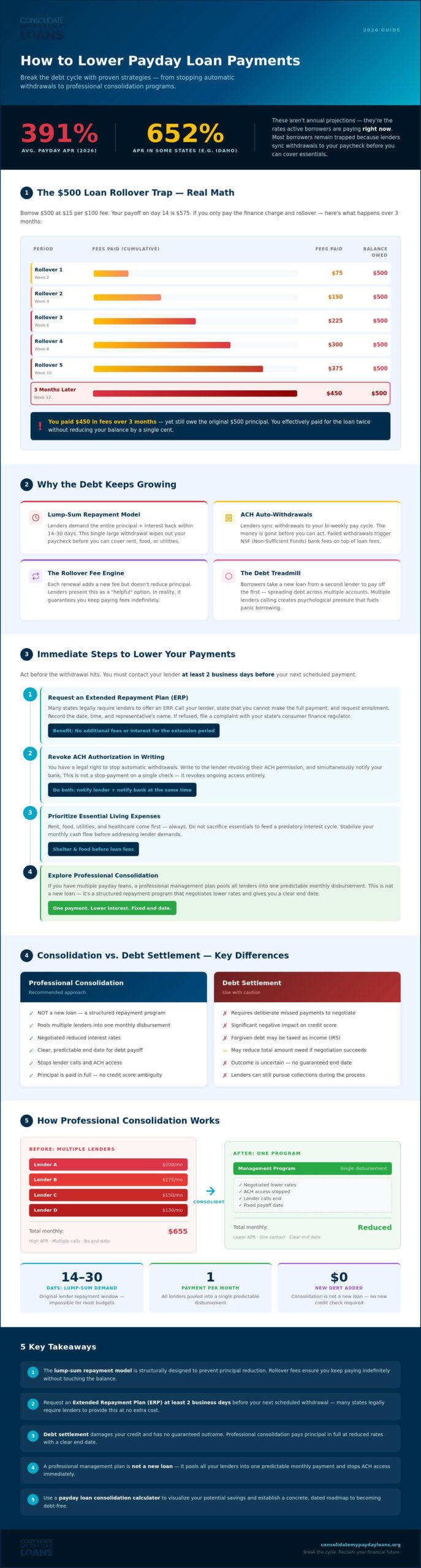

The Math of the 400% APR Trap

In 2026, the average APR for a Payday loan remains staggering at approximately 391%. In states like Idaho, that figure can skyrocket to 652%. Imagine borrowing $500 with a common fee of $15 per $100. On your next payday, you owe $575. If you can only afford the $75 finance charge, you “roll over” the loan. If you do this every two weeks for three months, you will have paid $450 in fees alone. Despite these heavy payments, you still owe the original $500. You’ve essentially paid for the loan twice without reducing the balance by a single cent. This is why paying only the minimum finance charge is a recipe for permanent debt.

How Rollovers Disguise Increasing Debt

Lenders often present a rollover as a helpful service. In reality, it’s a mechanism that transforms a short-term hurdle into a long-term trap. Each time you renew or roll over a loan, a new fee is tacked on. If your bank account lacks the funds when the lender attempts an ACH withdrawal, you face a cascade of Non-Sufficient Funds (NSF) fees from your bank. These additional costs make it even harder to lower payday loan payments in the future. Many borrowers find themselves in a “renewal trap,” where they take out a new loan from a different company just to pay off the first one. This creates a psychological “debt treadmill” that feels impossible to escape without a structured intervention.

Immediate Steps to Lower Your Monthly Payday Loan Burden

Facing a payday loan withdrawal that will leave your bank account empty is a terrifying experience. You don’t have to wait for the money to disappear. If you’re having trouble repaying your payday loan, the first step is to act quickly. You must contact your lender at least two business days before your next payment is due. This window is critical for initiating changes that can help you lower payday loan payments before they hit your balance. Your priority should always be your essential living expenses, like rent and food, rather than feeding a cycle of predatory interest. Taking control of your cash flow is the only way to stabilize your situation.

Requesting an Extended Repayment Plan (ERP)

Many states require lenders to offer an Extended Repayment Plan (ERP) or an Extended Payment Plan (EPP). These programs are designed to give you more time to pay without charging additional fees or interest for the extension. When you call your lender, stay calm but remain firm. State clearly that you’re unable to make the full payment and wish to enter an ERP. Document the date, the time, and the name of the representative you spoke with. If a lender refuses a legally required extension, you may need to file a complaint with your state’s consumer finance regulator. Taking this step is a powerful way to find payday loan relief and stop the immediate financial bleeding.

Regaining Control: Revoking ACH Authorization

You have a legal right to stop a lender from automatically withdrawing money from your bank account. This process is known as revoking ACH authorization. It’s different from a simple stop payment order on a single check. To do this, you must notify the lender in writing that you’re revoking their permission to access your account. Simultaneously, you should notify your bank. Most banks have a specific process for this, and they’re required by federal law to honor your request. Be prepared, however, for what happens next. Once the automatic withdrawals stop, the lender will likely start calling you aggressively. This is why having a structured plan to manage the debt is essential once you’ve secured your bank account. Stopping the drain on your account gives you the breathing room to evaluate professional help without the fear of an empty balance on payday.

Comparing Solutions: Payday Loan Consolidation vs. Debt Settlement

Choosing the right exit strategy to lower payday loan payments depends on your specific financial breaking point. Payday loan consolidation is the process of merging several high-interest obligations into one structured monthly payment. It’s a tool for recovery. In contrast, debt settlement involves negotiating with a lender to accept a single, smaller lump sum to satisfy the debt completely. While settlement might sound appealing, it usually requires you to stop payments entirely to gain leverage. This can severely damage your credit history for years and lead to aggressive collection efforts.

Consolidation is generally the superior choice if you still have a steady income but are drowning in the 300% to 600% APR fees common in the industry. It provides a way to pay back what you owe without the constant threat of new fees, which is often the most sustainable way to lower payday loan payments over the long term. Settlement is a last resort for those who are completely unable to pay anything. It effectively ends the relationship with the lender but leaves a significant mark on your financial record that can hinder future borrowing for housing or transportation.

The Benefits of Single-Payment Consolidation

A primary advantage of payday loan consolidation is the immediate simplification of your financial life. When you consolidate bills, you replace the chaos of multiple bi-weekly withdrawals with one predictable date. This organization provides psychological relief. It also establishes a fixed end date for your debt. Unlike the open-ended rollover cycles that can last for months, consolidation has a clear finish line. You can compare the nuances of these options in our detailed analysis: Debt Settlement vs. Consolidation for Payday Loans: Which Path Ends the Cycle?.

When to Consider Payday Loan Relief Programs

Professional relief programs act as a protective intermediary between you and aggressive collectors. These agencies employ professional negotiators who understand the lending industry’s pressure points. They work to reduce total balances and eliminate the predatory fees that keep your debt growing. They provide a buffer that stops the constant harassment. You must be cautious, though. The industry is unfortunately populated with companies that make unrealistic promises. Always verify that a relief agency is legitimate before sharing your financial details. A true advocate will focus on a sustainable path to recovery rather than quick, risky fixes that might leave you in a worse position.

How Professional Consolidation Lowers Your Payments Without New Debt

Many people believe the only way to escape high-interest debt is to borrow more money. This is a dangerous misconception that often leads to deeper financial trouble. Professional consolidation is not a new loan; it’s a structured debt management plan. It’s designed specifically to lower payday loan payments by restructuring the obligations you already have. Instead of juggling five different lenders with five different due dates, you work with an agency that pools your debts into a single disbursement account. This shift from chaos to order provides the stability you need to breathe again.

The primary mechanism for reducing your monthly burden is negotiation. Professional advocates contact your lenders to secure interest rate reductions and the waiver of predatory fees. For example, a borrower facing a crushing $1,200 monthly burden from multiple lenders can often see that restructured into a manageable $400 monthly plan. This dramatic reduction is possible because the plan focuses on paying down the principal balance rather than feeding the infinite cycle of 400% APR finance charges. You stop paying for the right to stay in debt and start paying for your freedom. To see how this could work for your specific situation, you can get started with a payday loan consolidation plan today.

The Consolidation Process: From Chaos to One Payment

The journey begins with a detailed consultation. A protective expert analyzes your total debt load against your actual take-home pay. Once a plan is established, the agency takes over the burden of communicating with your lenders. This means those relentless, high-pressure collection calls finally stop. Your advocate handles the friction so you can focus on your recovery. The final step is setting a new, single monthly payment that is mathematically aligned with your budget. This ensures you can meet your obligations without sacrificing essentials like groceries or utilities.

Why “No New Loan” Consolidation is Safer

Seeking a personal loan to pay off payday debt often fails for high-risk borrowers. If you’re already in a debt cycle, the only loans you likely qualify for carry high interest rates themselves. You end up swapping one trap for another. A management plan is safer because it requires no new debt and no high credit score for approval. It’s a path forward based on your ability to pay a fair amount, not your past credit mistakes. This methodology protects you from falling back into the “new loan” trap by focusing on total debt liquidation rather than just moving the balance around. You gain a clear end date and a partner in your financial recovery.

Choosing Your Path: Reclaiming Financial Control with Consolidate My Payday Loans

Breaking a cycle of high-interest debt requires more than just willpower. It requires a strategic partner who understands the mechanics of the lending industry and knows how to dismantle the traps set for consumers. At Consolidate My Payday Loans, we act as your dedicated advocate. We don’t just offer a service; we provide a stable anchor during financial turbulence. Our team creates a supportive, non-judgmental environment where your recovery is the only priority. We focus on the systemic problem while offering you the compassion you deserve.

You can begin your journey by using our Payday Loan Consolidation Calculator. This tool is designed to help you visualize exactly how much you can save by moving away from predatory rollovers. Seeing the numbers change from a mounting burden to a manageable plan often provides the first spark of hope. To get started, we follow a simple, three-step methodology: a comprehensive consultation, a deep analysis of your total debt load, and the implementation of a plan that provides immediate relief. Our goal is to lower payday loan payments so you can finally use your paycheck for your own needs.

Your Personalized Debt Exit Plan

Every financial situation is unique. Our specialists take the time to tailor a plan specifically to your income and your current list of lenders. We don’t believe in one-size-fits-all solutions. The simplicity of having just one monthly payment is a powerful tool for stress relief. It removes the mental fog caused by tracking multiple due dates and fearing the next bank withdrawal. Within the first 30 days of your program, you can expect the aggressive collection calls to stop as we take over the communication with your lenders. This breathing room is essential for long-term success.

Beyond Payday Loans: Credit Card Consolidation

Predatory lending practices aren’t limited to payday storefronts. Many individuals also struggle with high-interest credit card debt that carries similar risks of infinite interest. Our expertise extends to Credit Card Consolidation, allowing for a holistic approach to your financial health. By addressing all high-cost obligations simultaneously, we help you fix your entire financial picture rather than just patching one hole. This comprehensive strategy ensures that you regain your personal agency and stay out of debt for good. Stop the cycle of predatory lending and start your path toward psychological peace today.

Take Back Your Financial Future Today

You’ve learned how the lump-sum repayment model and rollover fees are specifically designed to keep you trapped in a cycle of debt. By revoking ACH authorization and seeking structured support, you can finally stop the unmanaged drain on your bank account. Working with a dedicated advocate is the most effective way to lower payday loan payments and replace predatory interest with a predictable path forward. You deserve the psychological peace that comes with knowing exactly when your debt will be gone.

Our expert payday loan relief specialists have been guiding individuals through these financial traps since 2004. Backed by the A+ rated support of our parent company, Solid Ground Financial, we offer the stability and insider knowledge required to dismantle complex debt. You can use our specialized payday loan consolidation calculator for an instant estimate of your potential savings. Don’t let another paycheck disappear into fees. Get a Free Debt Analysis and Lower Your Payments Today. Your journey toward financial recovery starts now, and we’re here to help you every step of the way.

Frequently Asked Questions

Can I lower my payday loan payments without a new loan?

Yes, you can lower payday loan payments without taking on new debt by entering a professional debt management program. These programs work by negotiating directly with your current lenders to reduce interest rates and waive predatory fees rather than issuing a new high-interest loan. This approach is often safer for those with low credit scores because it focuses on liquidating the original principal through a structured, single monthly disbursement plan.

What happens if I simply stop paying my payday loans?

Stopping payments without a plan usually triggers aggressive collection calls and multiple attempts by the lender to withdraw funds, leading to expensive bank NSF fees. While payday lenders rarely sue for small amounts, they often sell the debt to third-party collectors who may be more persistent. It’s always better to revoke ACH authorization and enter a structured relief program to protect your bank account and your psychological peace.

Is it possible to negotiate a lower settlement with a payday lender?

It is possible to negotiate a settlement where the lender accepts a lump sum that is less than the total balance. However, lenders usually only consider this after you’ve defaulted on payments for several months. While settlement can resolve the debt quickly, it often leaves a negative mark on your credit report. Consolidation is frequently a better middle ground for those who want to lower payday loan payments while stopping the interest trap.

How do I stop a payday lender from taking money out of my bank account?

You can stop automatic withdrawals by formally revoking your ACH authorization in writing to both the lender and your bank. Federal law requires banks to honor this request if you provide notice at least three business days before the scheduled transfer. Once you stop these withdrawals, it’s vital to have a professional management plan in place to handle the resulting collection efforts and negotiate a fair repayment structure.

Will consolidating my payday loans hurt my credit score?

A consolidation program may cause a minor, temporary dip in your credit score if you stop paying lenders directly during the transition period. However, the long-term impact is generally positive as your total debt decreases and you avoid the “default” status that comes with unpaid rollovers. Successfully completing a management plan demonstrates financial responsibility and removes the high-interest burden that often prevents borrowers from qualifying for traditional credit in the future.

What is an Extended Payment Plan (EPP) and how do I get one?

An Extended Payment Plan is a no-fee program that allows you to pay off your loan in smaller installments over a longer period. Many states require lenders who belong to industry trade groups to offer this option at least once per year. To get one, you must contact your lender at least one business day before the loan is due and formally request the extension. This is a critical first step to lower payday loan payments legally.

Can I consolidate both credit cards and payday loans together?

Yes, many professional programs allow you to combine both credit cards and payday loans into a single management plan. This holistic approach is often the best way to fix your entire financial picture by reducing high interest rates across all your unsecured debts. Consolidating everything into one payment simplifies your monthly budget and ensures that all your creditors are being handled by a single, professional advocate who understands the industry’s pitfalls.

How long does a payday loan consolidation program typically last?

Most payday loan consolidation programs are designed to be completed within 6 to 18 months, depending on your total debt amount and your monthly budget. Unlike the infinite cycle of bi-weekly rollovers, these programs provide a fixed end date for your debt from day one. This structured timeline allows you to see exactly when you’ll be debt-free, giving you a clear path toward reclaiming your financial agency and long-term stability.