Over 80% of payday loans are rolled over into new debt because the initial repayment terms are often impossible to meet. You’re likely feeling the weight of that statistic every time an automatic ACH withdrawal drains your bank account or another aggressive collector calls your phone. It’s a heavy burden to carry, and it’s not your fault that the system feels rigged against you. You are likely searching for payday loan payment plan options because you need a way out that doesn’t involve another high-interest cycle.

We understand the stress of watching your hard-earned money vanish before you can even pay your rent. This guide will show you how to stop the cycle of debt using extended payment plans and professional consolidation strategies that put you back in control. We will explore the legal “off-ramps” available in 2026, explain how to request an extended repayment schedule, and look at professional relief methods to protect your income from predatory withdrawals. You don’t have to face these lenders alone; there is a clear path toward regaining your financial agency.

Key Takeaways

- Learn how an Extended Payment Plan (EPP) legally breaks down a single impossible payment into smaller, predictable installments.

- Identify the specific payday loan payment plan options mandated by state laws to ensure you aren’t paying for rollovers you don’t need.

- Compare the total costs of different repayment methods to spot red flags before they lead to further financial strain.

- Follow a structured five-step checklist to communicate with lenders in writing and create a verifiable paper trail for your protection.

- Explore professional relief strategies for situations where lenders ignore your requests or refuse to offer fair terms.

What is a Payday Loan Payment Plan?

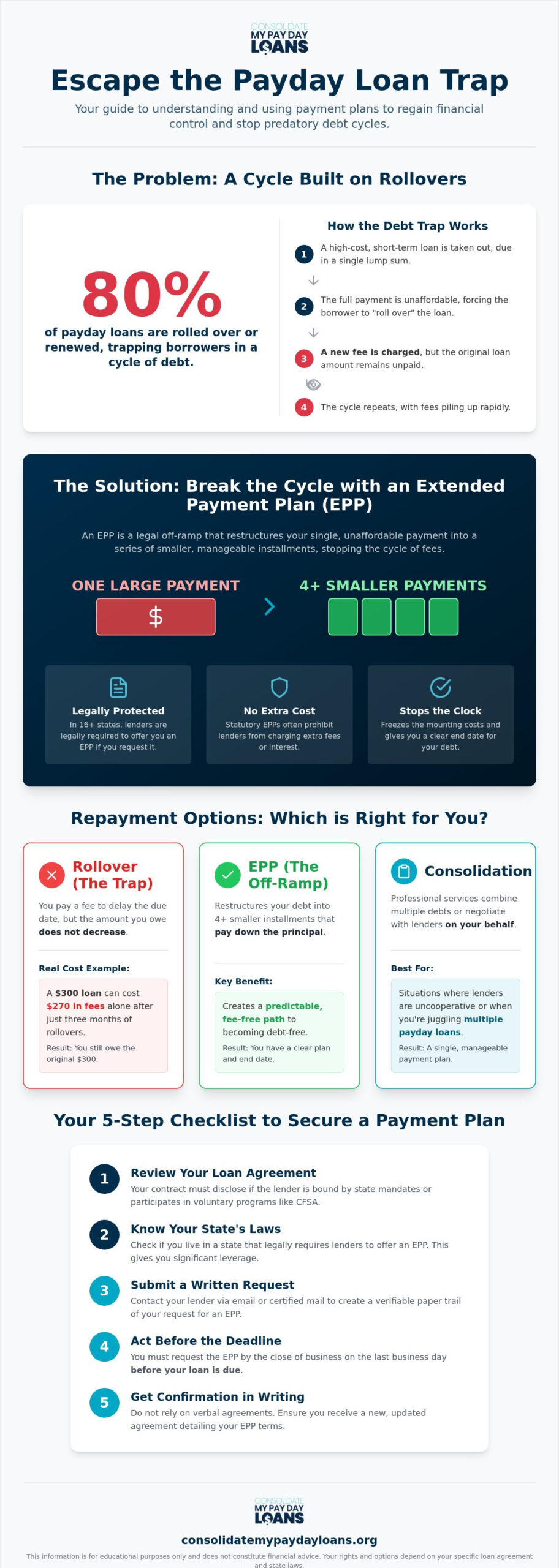

When you find yourself trapped in a cycle of high-interest debt, an Extended Payment Plan (EPP) acts as a vital off-ramp. To understand how these plans work, you first need to understand the mechanics of the debt itself. What is a payday loan? At its core, it’s a high-cost, short-term obligation designed to be repaid in a single lump sum on your next payday. However, for many of the 12 million Americans who use these loans annually, that single payment is impossible to make without sacrificing basic needs like rent or groceries. An EPP restructures that debt, breaking one large, overwhelming payment into a series of smaller, manageable installments over several weeks or months.

Lenders often hide these payday loan payment plan options from borrowers because they are far less profitable than the alternative. When you enter a payment plan, you are often protected from additional interest or late fees during the repayment period. In contrast, lenders prefer that you “roll over” the loan, which allows them to collect fees while the principal balance remains untouched. It’s important to distinguish between a voluntary plan, which a lender might offer at their own discretion, and a statutory plan. In at least 16 states, including Michigan and Florida, lenders are legally required to provide an EPP if a borrower requests it before the due date. These state-mandated plans are a powerful tool for regaining your financial agency.

The Problem with Payday Loan Rollovers

Rollovers are the primary engine of the debt trap. When you roll over a loan, you pay a fee to delay the due date, but not a single cent goes toward the actual money you borrowed. A rollover is a predatory trap that never reduces the principal balance. The math is devastating. With an average APR of 391%, a $300 loan typically carries a $45 fee every two weeks. If you roll that loan over for just three months, you will have paid $270 in fees alone, yet you still owe the original $300. This cycle is how a small cash advance quickly balloons into a thousand-dollar burden that feels impossible to escape.

How Payment Plans Stop the Debt Cycle

Choosing the right payday loan payment plan options can immediately freeze the mounting costs of your debt. By converting the balance into installments, you stop the clock on predatory fees and create a predictable monthly budget. Most plans allow you to spread the balance over 4 to 8 weeks, providing the breathing room needed to cover your essential living expenses. Beyond the financial benefits, there is a profound psychological peace that comes with having a clear, documented end date for your debt. You no longer have to fear the next payday; instead, you have a structured methodology for recovery and a direct path toward a debt-free life.

Common Payday Loan Payment Plan Options in 2026

Understanding your rights is the first step toward stopping aggressive collection calls. In 2026, payday loan payment plan options are largely dictated by where you live and the specific lender you chose. While the lending industry thrives on rollovers, state laws and industry trade groups have established frameworks to help you exit the debt cycle. Your specific loan agreement is the most critical document you own; it must disclose whether the lender participates in voluntary programs or is bound by state-specific mandates.

The Community Financial Services Association of America (CFSA) sets standards for many national lenders. Member lenders are generally required to offer an Extended Payment Plan (EPP) to borrowers who cannot meet their obligations. However, these standards are only as good as your knowledge of them. If you are struggling, seeking professional payday loan relief can help you navigate these often-obscure corporate policies. State regulations in places like Michigan and Florida provide even stronger protections, often mandating that lenders provide a path to repayment without adding more interest to the pile.

The Extended Payment Plan (EPP)

The EPP is the most common tool for debt recovery. It typically restructures your balance into four equal installments across your next four pay periods. One of the most important features of a statutory EPP is the “No-Cost” rule. In many states, lenders are strictly prohibited from charging extra fees or interest just for setting up the plan. This makes it a significantly better choice than a rollover. You must act quickly, though. Most lenders require you to request an EPP by the close of business on the last business day before your loan is due. If you miss this window, the lender may claim you are no longer eligible for these payday loan payment plan options.

Hardship Programs and Settlement Offers

Sometimes, an EPP isn’t enough to solve the problem. If you’ve experienced a significant life event, such as a job loss or a major medical emergency, you may qualify for a hardship program. These are internal lender policies that can lower your interest rate or extend your terms even further. Alternatively, you might negotiate a lump-sum settlement. This involves paying a single, smaller amount to satisfy the debt in full. While this can save you money, it often requires having a chunk of cash ready and can impact your credit score. If you feel overwhelmed by these negotiations, it might be time to explore professional consolidation to manage the process for you. Choosing between a structured plan and a settlement depends on your immediate cash flow and long-term financial goals.

EPP vs. Rollover vs. Consolidation: Which is Right for You?

Choosing between different payday loan payment plan options requires a clear-eyed look at your bank statement. While a rollover is almost always the most expensive path, the choice between a simple EPP and a comprehensive consolidation program depends on the complexity of your debt. A rollover adds fees without touching the principal balance; an EPP pauses the fees to let you pay the principal; consolidation restructures the debt entirely. You need to identify which tool fits your current financial reality before signing any new agreements or making another payment.

There are clear red flags that indicate a standard EPP won’t be enough to save you. If you are already juggling three or more separate lenders, or if your monthly debt payments exceed 50% of your take-home pay, a four-week extension won’t solve the underlying problem. In these cases, the “off-ramp” provided by an EPP is too short to prevent a financial crash. This is where payday loan consolidation becomes essential for long-term recovery. It moves beyond temporary extensions to address the systemic weight of high-interest debt by simplifying your obligations into a single, manageable structure.

When an EPP is the Best Choice

An EPP is often the ideal choice if you have only one loan and a temporary cash flow hiccup. If your income is stable but you just faced a one-time expense, these payday loan payment plan options provide the breathing room you need. It’s a far safer alternative than risking bank overdraft fees or taking out a second “bridge” loan. Success requires a disciplined budget for the next month, as you must be certain you can meet the four scheduled installments without fail to avoid falling back into the debt cycle.

When Consolidation is the Superior Option

Consolidation is the superior option for those caught in the “Multiple Loan Trap.” Verified research shows that 62% of borrowers take out a second payday loan within 30 days of their previous one. When you owe multiple lenders, managing separate EPPs becomes a logistical nightmare that often leads to missed payments and aggressive collection calls. Professional relief programs simplify this by negotiating across all your debts simultaneously. This results in a single monthly payment that fits your actual budget, protecting your bank account from the chaos of uncoordinated automatic withdrawals.

How to Request a Payment Plan: A 5-Step Checklist

Securing a repayment agreement requires more than just a phone call; it requires a methodical approach that protects your legal rights. Many borrowers fail to obtain payday loan payment plan options simply because they don’t use the correct terminology or follow up in writing. Lenders often train their representatives to push for rollovers first. You must be prepared to bypass these initial refusals by presenting a clear, documented case for your financial situation. If a lender remains uncooperative, employing specific predatory loan help strategies can help you assert your rights under state and federal consumer protection laws.

Step-by-Step Negotiation Guide

Follow this structured methodology to increase your chances of a successful negotiation:

- Step 1: Review your state laws. Determine if an EPP is mandatory in your state. Knowing that a lender is legally required to help you provides significant leverage during the conversation.

- Step 2: Contact the lender early. You must initiate the request at least 24 hours before your loan is due. Waiting until the day of the withdrawal often results in an automatic denial.

- Step 3: Use specific terminology. Ask specifically for an “Extended Payment Plan” or a “Hardship Plan.” Avoid vague requests for “help,” as these are often redirected toward high-cost rollovers.

- Step 4: Get it in writing. Never make a payment based on a verbal promise. Demand an amended loan agreement that outlines the new installment dates and amounts.

- Step 5: Document every interaction. Keep a log of who you spoke with, the date, and the specific terms discussed. This paper trail is vital if the lender later attempts to ignore the new agreement.

Revoking ACH Authorization

One of the most powerful tools you have is the right to stop a lender from pulling money from your account while you negotiate. You have the legal right to revoke automatic withdrawal permission at any time. To do this, you must notify the lender in writing and alert your bank that the authorization has been cancelled. Revoking your ACH authorization does not cancel your legal obligation to repay the debt, but it does grant you essential control over your monthly cash flow. This protection ensures that your rent and utility money isn’t seized while you are finalizing your payday loan payment plan options. If you need assistance managing multiple lenders who refuse to stop withdrawals, contact a consolidation expert to help secure your bank account today.

When Lenders Say No: Finding Professional Payday Loan Relief

Sometimes, even a perfectly executed negotiation fails to yield results. You might follow every step of the legal checklist only to have a lender flatly deny your request or claim they don’t offer payday loan payment plan options. This resistance is often a calculated tactic. Lenders understand that the longer they keep you in a state of financial uncertainty, the more likely you are to agree to another high-interest rollover just to stop the immediate pressure. DIY negotiation has significant limitations when you’re facing aggressive collectors who are trained to bypass your hardship claims and prioritize corporate profit over your financial recovery.

Professional payday loan relief provides the stable anchor you need when the lending industry becomes overwhelming. Instead of you fighting these battles alone, a dedicated advocate acts as a buffer between you and the lender’s collection department. This professional intervention stops the cycle of predatory withdrawals and ends the constant harassment. By shifting the conversation from emotional stress to structured financial recovery, you gain the breathing room necessary to focus on your long-term goals rather than just surviving until the next Friday.

The Power of Professional Advocacy

A professional consolidation service uses deep industry knowledge to challenge lender tactics that individual borrowers might not recognize as unfair or illegal. These programs do more than just ask for extensions; they restructure your debt entirely. Consolidate My Payday Loans uses this expertise to stop lender harassment and simplify your financial life instantly. By merging multiple high-interest payday loans and even credit card debt into a single, manageable framework, you can finally move from a state of “surviving” the debt cycle to actually paying off the principal balance for good. You regain personal agency over your income, ensuring that your money stays in your bank account where it belongs.

Your Next Steps for Financial Peace

The first step toward regaining control is understanding the numbers. Using a payday loan consolidation calculator allows you to see the tangible benefits of a structured recovery plan compared to the endless fees of rollovers. Waiting usually makes the situation worse, as interest continues to compound and lenders become more aggressive with their collection efforts. You don’t have to wait for a lender’s permission to find payday loan payment plan options that actually work for your budget. Taking action now protects your bank account and provides the psychological peace that comes with a clear path out of debt. Contact us today to explore your consolidation and relief options.

Take Control of Your Financial Future Today

Breaking free from high-interest debt requires a shift from passive stress to active management. You now understand that payday loan payment plan options exist as legal safeguards to stop the cycle of rollovers and predatory withdrawals. Whether you utilize a state-mandated EPP or choose to revoke your ACH authorization, the power to protect your income is in your hands. These tools are the first step toward regaining your financial agency and ending the chaos of uncoordinated withdrawals.

If lenders continue to ignore your rights, you don’t have to fight them alone. With over 20 years of expertise through Solid Ground Financial, we provide the expert advocacy needed to silence aggressive collectors for good. You can use our specialized payday loan consolidation calculator to estimate your savings and see exactly how much you can simplify your monthly budget. It’s time to stop surviving payday to payday and start building a stable foundation for your future. Start your journey to debt-free living with a free consolidation consultation. You deserve the psychological peace that comes with true financial stability.

Frequently Asked Questions

Can a payday lender refuse to give me a payment plan?

A lender’s ability to refuse depends entirely on your state’s specific consumer protection laws. In at least 16 states, including Michigan and Florida, lenders are legally required to provide an EPP if you make the request before the loan’s due date. In states without these mandates, lenders can technically refuse your request and may try to steer you toward a high-interest rollover instead.

Do I have to pay a fee to start an extended payment plan?

In most states that mandate payday loan payment plan options, lenders are prohibited from charging any additional fees or interest for the extension. This “No-Cost” rule is a vital protection designed to help you exit the debt cycle without increasing your balance. You should always verify your amended loan agreement to ensure the lender hasn’t hidden any “processing fees” in the new terms.

How many times can I use an extended payment plan for the same loan?

Most state regulations and industry standards limit borrowers to one EPP per 12-month period with a specific lender. These plans are intended as a one-time “off-ramp” for temporary financial turbulence. If you find yourself needing an extension for every loan you take out, it’s a clear indicator that a more comprehensive consolidation strategy is necessary to address the systemic debt.

Will a payday loan payment plan hurt my credit score?

Entering a payment plan typically does not hurt your credit score because most payday lenders don’t report to the three major credit bureaus. Successfully completing a plan is actually a protective measure for your credit. It prevents the debt from being sold to a collection agency, which is the point where payday debt usually begins to appear on and damage your credit report.

What is the difference between a payment plan and a loan rollover?

A payment plan is a structured path to zero, while a rollover is a mechanism for staying in debt. In a payment plan, your installments go toward reducing the principal balance. In a rollover, you pay a fee just to delay the due date, meaning the amount you owe doesn’t decrease at all. One is an exit strategy; the other is a debt trap.

Can I stop automatic withdrawals if I am on a payment plan?

Yes, you have the legal right to revoke your ACH authorization at any time, regardless of whether you are on a repayment plan. This action puts you back in control of your cash flow and ensures that essential expenses like rent are covered. You must notify the lender in writing and alert your bank that you have officially withdrawn your consent for automatic withdrawals.

What should I do if I cannot afford the payments on my new plan?

If the installments in your new plan are still unmanageable, you should seek professional relief immediately. Missing a payment on a restructured plan often voids the agreement and triggers aggressive collection calls or legal action. Professional advocates can help negotiate a more realistic monthly payment that aligns with your actual income and protects you from further financial turbulence.

Is debt consolidation the same as a payment plan?

No, they are distinct strategies. A payment plan is a single-lender agreement to extend one specific loan. Consolidation is a more robust methodology that merges multiple high-interest debts into one new, simplified structure with a single monthly payment. Consolidation is often the superior choice for individuals who are struggling to manage several different payday loan payment plan options at once.