Reviewed by Nela Diaz — Negotiations Manager, Solid Ground Financial. [Last reviewed: July 9, 2026]

Imagine waking up on payday only to find your bank account already empty because an automatic withdrawal claimed your entire paycheck before you could buy groceries. If you are struggling with interest rates exceeding 400% APR and aggressive collection calls, you are likely looking for predatory loan help to stop the cycle. It is exhausting to feel like you are drowning while lenders use the fear of legal action or jail time to keep you trapped in a loop of debt.

You don’t have to face this pressure alone. This guide will teach you how to identify deceptive lending tactics, exercise your legal consumer rights, and implement a proven exit strategy to stop rollovers for good. We will show you how to reduce the total amount you owe and consolidate multiple payments into one manageable monthly installment so you can finally regain your financial agency and find the peace of mind you deserve.

Key Takeaways

- Identify the “Triple-Digit Trap” and the specific red flags that signal a lender is using abusive terms to keep you in a cycle of debt.

- Exercise your legal right to revoke ACH authorization and stop automatic bank withdrawals that leave you without money for essentials.

- Evaluate the differences between consolidation, settlement, and bankruptcy to determine which strategy will reduce your total debt most effectively.

- Follow a clear, 5-step roadmap for predatory loan help designed to consolidate multiple high-interest payments into one manageable monthly installment.

- Learn how professional payday loan relief can end the cycle of aggressive collection calls and restore your psychological peace.

Identifying the Red Flags: What Makes a Loan Predatory?

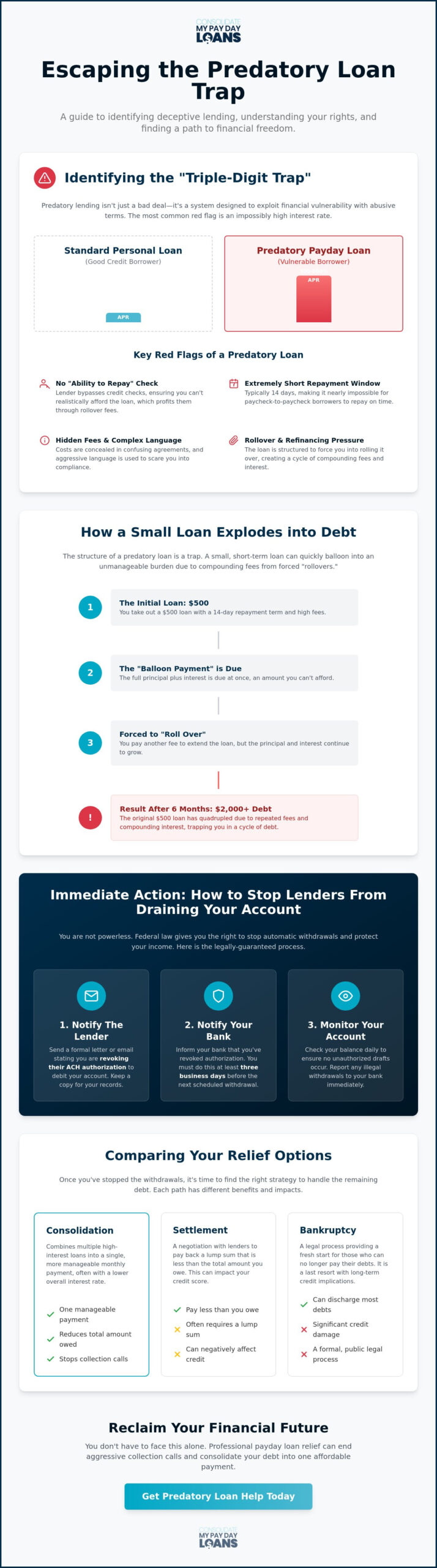

Predatory lending isn’t just a bad deal; it’s a systemic practice designed to exploit your financial vulnerability through abusive terms. You might wonder, What is predatory lending? At its core, it’s any lending practice that uses deceptive or unethical means to convince you to accept a loan that you cannot realistically afford. These lenders don’t care about your long-term stability. They care about the interest. With total household debt reaching $18.8 trillion in late 2025, more people are finding themselves targets of these aggressive tactics.

The most common red flag is the “Triple-Digit Trap.” While a standard personal loan for a borrower with good credit might carry an interest rate between 12% and 13.5% in 2026, predatory lenders often charge APRs ranging from 300% to 600%. They bypass traditional credit checks and skip “Ability to Repay” (ATR) assessments. This is intentional. If they knew you could pay the loan back in full, they wouldn’t make as much money from the fees associated with rollovers. They want you to stay in debt. It’s a psychological game where they keep you in a state of perpetual panic, making you feel that seeking predatory loan help is your only option to survive the week.

The Anatomy of a Predatory Payday Loan

Most predatory loans are structured around a very short repayment window, usually just 14 days. This timeline is often impossible for a borrower already living paycheck to paycheck. Because the “balloon payment” requires the entire principal and interest to be paid at once, many people are forced to roll the loan over into a new one. This is where the costs explode. A simple $500 loan can easily balloon into a $2,000 debt in just six months due to compounding fees and interest. The structure ignores your actual budget and focuses solely on draining your next paycheck. Understanding your payday loan payment plan options before you sign can help you avoid this trap entirely.

Deceptive Marketing and Concealed Fees

Lenders often hide the true cost of borrowing behind complex language and digital profiling. They target vulnerable populations by analyzing online behavior to find people in urgent need of cash. Once you’re in their system, you might encounter “hidden” fees that weren’t mentioned in the initial pitch. Agreements often include aggressive or threatening language designed to scare you into compliance. If you feel overwhelmed by these tactics, remember that professional predatory loan help exists to guide you through the process of reclaiming your financial agency. You don’t have to navigate this alone.

Immediate Action: How to Stop Predatory Lenders from Draining Your Account

The moment you realize a lender is draining your bank account, a deep sense of panic often sets in. You see your hard-earned money disappear before you can pay rent or buy groceries. It’s a terrifying experience, but you aren’t powerless in this situation. You have specific legal rights designed to protect your income from aggressive drafting tactics. Taking immediate action is the first step toward getting the predatory loan help you need to stabilize your finances and stop the bleeding.

Revoking Your ACH Authorization Legally

Revoking your ACH (Automated Clearing House) authorization is a federal right guaranteed under the Electronic Fund Transfer Act. This means you can tell a lender they no longer have permission to take money from your account, regardless of what the original loan contract says. To do this effectively, follow these three steps:

- Notify the lender in writing: Send a formal letter or email stating that you are revoking their authorization to debit your account. Keep a copy of this communication for your records.

- Notify your bank: Call your bank and inform them you’ve revoked authorization for that specific lender. You should do this at least three business days before the next scheduled transfer.

- Monitor your account: Check your balance daily to ensure no unauthorized drafts occur.

It’s vital to understand the difference between a “Stop Payment” order and revoking authorization. A stop payment usually targets one specific check or transaction and often carries a bank fee. Revoking authorization is a broader command that terminates the lender’s right to access your account entirely. If you’re feeling overwhelmed by the process, seeking professional payday loan relief can help you manage these communications more effectively.

Dealing with Aggressive Collection Tactics

Once the automatic drafts stop, lenders often pivot to aggressive collection calls. The Fair Debt Collection Practices Act (FDCPA) protects you from harassment, even if you owe the money. Lenders cannot call you at unreasonable hours, use profanity, or lie about the legal consequences of your debt. A common scare tactic involves threatening you with jail time. In the United States, you cannot be sent to jail for a civil debt like a payday loan. It’s a hollow threat used to exploit your fear.

When a collector calls, keep it simple. Use a script like this: “I am aware of this debt. I am requesting that you cease all telephone communication and only contact me in writing at my mailing address.” If the lender continues to attempt “micro-drafts” or small unauthorized charges to test your account, the most secure move is to open a new bank account at a different institution. This creates a clean break and ensures your next paycheck is safe while you work on a long-term resolution. Getting predatory loan help starts with securing your current income first.

Comparing Relief Options: Consolidation vs. Settlement vs. Bankruptcy

Choosing the right path for predatory loan help is a pivotal moment in your financial recovery. You’re likely weighing the benefits of consolidation, the risks of settlement, and the finality of bankruptcy. Each option carries distinct consequences for your credit score and long-term stability. It’s not just about stopping the aggressive calls today; it’s about ensuring you don’t fall back into the same trap tomorrow. Understanding these mechanics allows you to move from a place of panic to a position of power.

Payday Loan Consolidation: The Single Payment Solution

Consolidation is often the most stable path for individuals juggling multiple high-interest debts. It works by combining your various obligations into one lower monthly payment that fits your actual budget. This process effectively closes the “rollover loop” where you pay fees without ever touching the principal. Instead of watching your balance grow despite your payments, your money finally begins to reduce what you owe. You can use our Payday Loan Consolidation Calculator to estimate your potential savings and see a clear timeline for your debt-free date.

Many people mistakenly believe they need a “new loan” to consolidate. If your credit is already damaged by high-cost debt, taking out a new personal loan is often a mistake. These new loans frequently come with their own high interest rates or hidden fees, simply moving the problem from one lender to another. True consolidation focuses on restructuring your existing debts through a structured management plan, allowing you to regain control without adding more interest to your life. If you are currently trapped in a rollover cycle, exploring extended repayment and payday loan payment plan options can provide a structured off-ramp before your debt grows further.

Debt Settlement: Negotiating for Less Than You Owe

Settlement involves negotiating with lenders to accept a lump sum payment that is less than the total balance. While this sounds appealing, it can be extremely risky for those without significant cash savings. Lenders aren’t required to settle, and they may continue aggressive collection efforts while you try to save up a lump sum. Additionally, the IRS often views forgiven debt as taxable income. You might receive a 1099-C form and find yourself owing the government money at the end of the year.

Bankruptcy remains a last resort for those whose debt has become completely unmanageable. While it provides a fresh start, it comes with high costs. Based on June 2026 data, attorney fees for Chapter 7 or Chapter 13 can range from $1,500 to $3,500. A court filing stays on your credit report for up to ten years, which can impact your ability to rent a home or find certain types of employment. Professional predatory loan help through consolidation offers a middle ground, providing relief and reduced rates without the extreme long-term fallout of a bankruptcy filing.

Step-by-Step Guide to Consolidating Predatory Loans

Moving from the crushing weight of debt to a structured repayment plan requires a tactical, disciplined approach. You’ve already learned your rights and how to stop unauthorized drafts. Now, it’s time to build a bridge toward financial freedom. This process begins with total transparency. You cannot fix what you haven’t measured, and getting effective predatory loan help depends on having a complete picture of your financial landscape. By following a methodical roadmap, you can move from feeling trapped to being consolidated.

Inventory Your Debt and Income

Your first step is to create a comprehensive list of every obligation. Don’t leave anything out. This list should include:

- The name of every lender and their contact information.

- The current balance and the original principal amount.

- The APR, which often exceeds 400% in these high-cost traps.

- Your next due date and the specific method the lender uses for collection.

Be sure to look for “hidden” debt. Many people overlook cash advance apps like Dave or Earnin, which can contribute to the same cycle of dependency as traditional payday loans. Once your list is complete, calculate your discretionary income. This is the amount left over after you pay for absolute essentials like rent, utilities, and food. This number is the foundation of your new, manageable monthly installment. It represents what you can realistically afford to pay without falling behind on your basic needs again.

Selecting a Legitimate Relief Partner

With your inventory ready, you must choose a partner to help you navigate the negotiation process. The industry is unfortunately full of “scam” relief programs that target people in distress. To protect yourself, look for companies with a long-standing reputation and a proven history of consumer advocacy. A legitimate partner will never demand large upfront fees before they have performed any work. Federal law prohibits debt relief companies from charging fees until they have successfully negotiated a settlement or restructured your debt.

The transition period is often the most stressful part of the journey. This is the gap between stopping your payments to predatory lenders and officially starting your consolidation plan. During this time, lenders may increase their collection efforts. Having a professional advocate handle these communications is essential for your psychological peace. If you are ready to stop the cycle, you can apply for payday loan relief to begin your five-step journey toward a zero balance. A clear program should always offer a definitive end date for your debt rather than keeping you in perpetual payments. This structured approach ensures you are guided rather than overwhelmed.

Reclaiming Your Future: Life After Predatory Debt

Escaping the cycle of high-interest lending is about more than just settling a balance; it’s about reclaiming your mental health and personal agency. When you finally secure the predatory loan help you’ve been searching for, the most immediate change isn’t just financial. It’s the silence. The aggressive collection calls stop. The fear of checking your bank account on payday disappears. This transition marks the beginning of your recovery, moving you from a state of constant survival into a structured, manageable plan for long-term stability.

Psychological peace is a tangible benefit of professional debt intervention. When you aren’t constantly worried about interest rates exceeding 400% APR or unauthorized bank drafts, you can focus on your family and your career. We act as a stable anchor during this time, providing a supportive and non-judgmental environment where your recovery is the priority. Our goal is to lead you toward a credit-healthy future where you never have to rely on a high-cost lender again.

How Consolidate My Payday Loans Works for You

As your dedicated advocate, we step between you and the lenders who have been draining your resources. Our process involves negotiating directly with your creditors to lower or even eliminate the interest that keeps you trapped. We use our industry knowledge to push for terms that reflect your actual ability to pay. This removes the burden of dealing with hostile collectors and puts the power back in your hands. You don’t have to argue with lenders who use intimidation tactics; we handle the difficult conversations for you.

The “Single Payment” benefit is a cornerstone of our payday loan relief programs. Instead of tracking multiple due dates and risking overdraft fees, you make one monthly installment to us. We then handle the distribution to your various lenders. This approach stops the chaotic ACH cycle and ensures your bank account is protected from the micro-drafting attempts discussed earlier. It simplifies your life and provides a clear, predictable path to a zero balance.

Building a Financial Firewall

Once your payday loans are under control, it’s time to build a firewall against future financial turbulence. Start by setting aside a small amount each month for an emergency fund. Even a few hundred dollars can prevent a minor car repair or medical bill from turning into a reason to seek another high-interest loan. This fund is your first line of defense, ensuring you remain independent from predatory practices. If you still have other high-interest obligations, you might consider Credit Card Consolidation to further streamline your finances and lower your overall interest costs.

Your journey to financial freedom is a marathon, not a sprint. By following a structured methodology and staying committed to your new budget, you can rebuild your credit score and regain your status as a confident consumer. The debt trap is designed to feel permanent, but with the right guide, it’s entirely escapable. Start your path to financial peace today and leave the stress of predatory debt behind for good.

Take Control of Your Financial Narrative

Breaking free from high-interest debt requires a combination of legal knowledge and tactical action. You now understand how to revoke ACH authorizations to protect your bank account and why consolidation is a superior alternative to the cycle of rollovers. Regaining your personal agency isn’t just about the numbers; it’s about the psychological peace that comes with having a clear, structured path forward. Seeking predatory loan help is the most decisive step you can take to stop the harassment and start your recovery.

Consolidate My Payday Loans has been a stable anchor for borrowers since 2004. Our specialized payday loan relief programs are specifically designed to stop the cycle of debt for good. We provide expert negotiators who deal directly with predatory lenders on your behalf, ensuring you are no longer fighting this battle alone. You’ve been through enough stress. It’s time to let a protective expert handle the burden so you can focus on building a stable future.

Calculate your potential savings and escape the debt trap now. You don’t have to live in fear of the next payday. A life of financial freedom and stability is within your reach.

Frequently Asked Questions

Can I go to jail for not paying back a payday loan?

No, you cannot go to jail for failing to repay a payday loan. This is a civil debt, and the United States abolished debtors’ prisons long ago. Lenders often use the threat of criminal charges or arrest as an intimidation tactic to force you into making a payment. If a collector makes these threats, they are likely violating the Fair Debt Collection Practices Act, and you should report them to the Consumer Financial Protection Bureau.

How do I stop a payday lender from taking money out of my bank account?

You stop automatic withdrawals by revoking your ACH authorization in writing. Send a formal notice to the lender stating you’ve terminated their access and provide a copy of this letter to your bank at least three business days before your next payday. If the lender continues to attempt drafts, you may need to place a formal stop payment order on that specific merchant or consider opening a new account to ensure your income is protected.

What is the maximum interest rate a lender can legally charge?

There is no single federal interest rate cap for all lenders; however, federal credit unions are limited to 18%. State laws vary significantly. Some states have implemented 36% caps to protect consumers, while others, like Mississippi, have laws allowing APRs over 300% until July 2030. You should check your specific state’s regulations to see if your lender is exceeding the local legal limits for installment or payday loans.

Will payday loan consolidation hurt my credit score?

Payday loan consolidation typically has a neutral to positive impact on your credit score over the long term. While you might see a slight initial dip if you stop payments to lenders during the transition to a new plan, the consistent payment history and reduction in total debt will help rebuild your score. This structured approach is far less damaging than defaulting entirely or facing the long-term fallout of a bankruptcy filing.

What happens if I just stop paying my payday loans?

If you stop paying without a structured plan, you will face aggressive collection calls, potential lawsuits, and significant damage to your credit report. Lenders may also sell your debt to third-party collectors who can be even more persistent. Instead of ignoring the problem, seeking professional predatory loan help allows you to resolve the debt through negotiation while protecting your rights and stopping the cycle of harassment.

How long does it take to get out of the payday loan cycle with consolidation?

Most borrowers can successfully exit the payday loan cycle within 6 to 18 months through a structured consolidation program. The exact timeline depends on the total amount of debt you’ve accumulated and what you can realistically afford to pay each month. Unlike the endless loop of rollovers and fees, this method provides a clear, predictable end date that helps you regain control of your financial life.

Are there government programs for payday loan relief?

There are no specific government programs that pay off your payday loans, but federal and state agencies offer resources to protect your rights. The Consumer Financial Protection Bureau (CFPB) handles complaints against abusive lenders and enforces consumer protection laws. While the government doesn’t provide direct cash for debt, seeking professional predatory loan help can help you utilize these legal protections to negotiate better terms and stop abusive practices.

Can I consolidate payday loans with bad credit?

Yes, you can consolidate payday loans even if you have a low credit score. Unlike traditional personal loans that require high FICO scores for approval, consolidation programs focus on your current ability to manage a single monthly payment. These programs restructure your existing debt rather than issuing a new high-interest loan, making them an accessible option for individuals who are already facing financial turbulence and need a stable path forward.